What Is Euler’s Number?

What makes an exponential an exponential? Are any exponentials more special than others? And what does Euler’s number have to do with any of this? Stay tuned for the answers.

Jason Marshall, PhD

Listen

What Is Euler’s Number?

Have you ever noticed that little ex button on your super fancy scientific calculator? Have you ever wondered what it means and what it’s used for? As it turns out, the story of the symbol on that little key is a surprisingly interesting one. Particularly because the principal player—the magnificent number e (also known as Euler’s number)—is one of the most famous numbers in the world of math … right up there with π, the golden ratio, and the imaginary unit, i, that we recently discussed.

So what’s the deal with Euler’s number? What are some of its fascinating properties? And what does it have to do with the idea of exponential growth that we talked about last time? Keep on reading to find out.

An Interesting Question

If you were to take $1 and invest it in an account offering 100% interest per year, how much money would you have at the end of the year?

If you were to take $1 and invest it in an account offering 100% interest per year, how much money would you have at the end of the year? If you think about it, you’ll see that the answer isn’t well defined. Why? Well, if it’s a lousy investment, the bank or whomever you’ve made the investment with will hold your $1 for the entire year and then at the last possible instant of the last possible second add another $1 to your account. In other words, in this rather “bad” investment (I hesitate to really call it bad since earning 100% interest is pretty much always a too-good-to-be-true deal), you earn the entirety of your interest payment all at once at the end of the year. Why is this bad?

To see, let’s imagine a more generous bank that pays you 100% / 12 = 8.33% interest on your initial $1 investment on the first day of every month. In this case, at the end of the first month, you’d have your original $1 plus the $1 • 0.0833 = $0.0833 for a total of about $1.08. At the end of the second month you’d again have your original $1 plus this new approximately 8 cents (from the first month) plus another roughly 8 cents for the second month’s interest. If we continue to play this game for each of the 12 months of the year, you’ll find that you’d end up with $1 + (12 • $0.0833). If you do the math and forgive the bit of rounding error that’s accumulated over the course of our calculation, you’ll find that you’d end up with a grand total of $2 in your account.

But wait … that’s no better than before! Indeed, it’s not—but that’s because we made a mistake in our thinking. Can you spot what we forgot? If not, take a minute and think about what we did with each month’s interest during subsequent months. We did … nothing, right? But that was wrong—because the interest we made every month should have been accruing interest of its own!

An Even More Interesting Question

To see what I mean, let’s continue thinking about our investment with monthly interest payments. As we calculated earlier, at the end of the first month our investment would be worth about $1.08. Now (here’s the part where we messed up before), during the second month we should accrue 8.33% interest not just on the original $1, but on the entire newly updated $1.08 value of our account. So at the end of the second month we would have the $1 that we started with plus 8.33% • $1 in interest for each of the first two months plus the extra 8.33% • (8.33% • $1) in interest that we earn off of the first month’s interest during the second month. Make sense? If you add all of this up, you’ll find that our investment would be worth a total of about $1.17 at the end of two months … which is a whopping 1 penny more than the $1.16 that we would have calculated using our earlier method which ignored compounding interest on top of interest.

Well that’s only a penny, you’re thinking—who cares about a penny?! While the difference is only a penny right now, month after month the differences will add up. And if we carry this entire calculation through to the end keeping track of the interest earned by interest all along the way, at the end of the year your $1 investment will have grown to $2.61 … which is a fair bit more than the $2 we incorrectly calculated before. So, as you can see, compounding interest really does make a difference!

Introducing Euler’s Number

Why not accrue interest every teeny tiny fraction of a second?

But, you might be thinking, why did we choose to accrue interest every month … why not every week? Or every day? Or every hour … minute … or second? Or, if we really want to get crazy (and of course we do), why not accrue interest every teeny tiny fraction of a second? Or, since I’ve ran out of ways to describe breaking time down any further, why not accrue interest continuously?

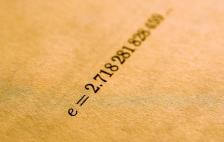

OK, let’s give it a whirl. If we break our interest payments into 52 weekly installments, we end up with roughly $2.69 at the end of the year—that’s about $0.08 more than we make by accruing monthly. If we choose 365 daily interest payments instead, we end up with about $2.715—only $0.025 more. As you can hopefully see and feel, we’re approaching some kind of limit here … a point of diminishing returns where dividing the interval up into smaller and smaller pieces is yielding less and less additional interest. Long ago, some clever math fan played around with exactly this calculation and found that if you take this exercise to its logical conclusion and accrue interest continually, you end up at the end of the year with $2.718281828459045… (the dots represent the fact that this number is actually irrational and thus doesn’t cease). And, it turns out, that is the very same number that is now known as Euler’s number.

The Natural Exponential

This number—Euler’s number—usually represented by the letter e, is sometimes called the natural exponential. As we talked about last time, any expression that looks like 2x, 3x, 10x, or anything else raised to some power (which we’re calling x) represents what’s called an exponential and exhibits the kind of rice-on-the-chessboard exponential growth that we looked at.

But Instead of the base 2, 3, or 10, it turns out that the base approximately equal to 2.71828—in other words, e—shows up all over the place in the world of math and science. Take a look through any calculus or physics book, and you’ll find things that look like ex all over the place. In our example, the formula ex tells us the amount of money you would have after investing $1 for x years in an amazing account offering continual 100% growth. In the rest of the natural world, numerous variations of this same formula can be found modeling the exponential growth of all sorts of things. From the populations of humans and bacteria to the worlds of economics and finance, Euler’s number is a mathematical rock … and a mathematical rock star to boot.

Wrap Up

OK, that’s all the math we have time for today.

For more fun with math, please check out my book, The Math Dude’s Quick and Dirty Guide to Algebra. And remember to become a fan of The Math Dude on Facebook, where you’ll find lots of great math posted throughout the week. If you’re on Twitter, please follow me there, too.

Until next time, this is Jason Marshall with The Math Dude’s Quick and Dirty Tips to Make Math Easier. Thanks for reading, math fans!

Euler’s number image from Shutterstock.

About the Author

Jason Marshall is the author of The Math Dude’s Quick and Dirty Guide to Algebra. He provides clear explanations of math terms and principles, and his simple tricks for solving basic algebra problems will have even the most math-phobic person looking forward to working out whatever math problem comes their way.